Sell Your House Before a Tennessee Foreclosure — Power-of-Sale and Why Speed Matters

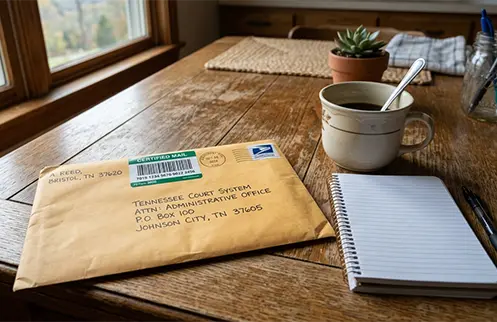

The mail you do not want to open is usually the mail you have to.

If you are behind on your mortgage in Kingsport, Johnson City, Bristol, or anywhere across Northeast Tennessee, the certified envelope is not a mistake and it is not a scare tactic. Tennessee uses a power-of-sale foreclosure process — meaning a trustee, not a judge, runs the sale — and the timeline is faster than most people realize. From the first published notice to the sale on the courthouse steps can be as short as twenty days, and once the gavel falls, you generally cannot get the home back.

We're Korey Whitley and Evan, the owners of Whitley Hamilton Home Buyers. I'm Korey — born and raised in Kingsport, with more than ten years buying homes across the Tri-Cities. We are not a national brand running ads from another state. We are your neighbors. And the reason this page exists is simple: we believe the people facing a Tennessee foreclosure deserve to know exactly how the clock works, what their real options are, and how to make a decision before the trustee sale date — when the most options are still on the table.

Selling your home to a cash buyer is one of those options. It is not the only one, and it is not always the right one — but it is often the cleanest path to ending the debt, keeping any remaining equity, and walking away with dignity and your credit less damaged than after a completed foreclosure. We close in as little as seven to fourteen days, as-is, with no commissions and no fees. Below is the honest, plain-language version of how Tennessee foreclosure actually works and where a cash sale fits.

Get Your Free Cash Offer Now!

Fill out this form to get your no-obligation all cash offer started!

Get Your Free Offer TODAY!

Fill In This Form To Get Your No-Obligation All Cash Offer Started!

Probate, Paperwork, and Possession Can Be Overwhelming

Tennessee foreclosure law sits in the Tennessee Code at Tenn. Code Ann. § 35-5-101 et seq., and it is one of the fastest non-judicial foreclosure processes in the country. The deed of trust you signed at closing almost certainly contains a 'power of sale' clause — the clause that lets the lender appoint a trustee and conduct a public auction without going to court. That is why there is no judge involved, no lawsuit to defend, and no automatic courtroom protection.

Here is the basic Tennessee sequence, with the specific statutes the lender's trustee has to follow:

- Default and federal waiting period. Once you fall behind, federal mortgage-servicing rules generally prevent the lender from initiating foreclosure during the first 120 days of delinquency. This buys you time to apply for loss mitigation.

- 60-day owner-occupied notice (§ 35-5-117). For an owner-occupied home, the lender or trustee must send you a notice of the right to foreclose at least 60 days before the first newspaper publication.

- Newspaper publication (§ 35-5-101). The notice of sale must be published in a county newspaper three times, with the first publication at least 20 days before the sale.

- Certified-mail notice (§§ 35-5-101, 35-5-104). The trustee must send a copy of the foreclosure notice to you by certified or registered mail on or before the first publication date.

- Online posting (§ 35-4-104, effective July 1, 2025). Notices are now also posted online at foreclosuretennessee.com through a third-party service.

- Trustee sale. The auction is held at the county courthouse on the date in the published notice. The lender usually makes a credit bid for what is owed.

From the first missed payment to the sale on the courthouse steps, Tennessee's process commonly runs about five to six months — but the active foreclosure window, once notice begins, can be as short as twenty days from the first publication.

The Hardest Truth — and Why It Should Change How You Act

This is the single most important sentence on this page. In Tennessee, once a non-judicial trustee sale completes, you generally cannot get the home back. The Tennessee Code provides a two-year redemption right in §§ 66-8-101 through 66-8-103, but standard deeds of trust nearly always expressly waive that right. Pull out your deed of trust and look — most owners' redemption rights are gone before the sale ever happens.

Tennessee also no longer recognizes 'wrongful foreclosure' as a standalone legal claim, following a Tennessee Supreme Court ruling. That makes the path to undoing a completed sale even narrower than in many states. The practical implication is straightforward: every option you have lives on this side of the sale date. After it, almost none of them remain. That is why a clear-eyed look at your options — including selling to a cash buyer who can close before the sale — needs to happen now, not after.

Your Real Options Before the Sale

Loss mitigation with the lender. Loan modification, repayment plan, forbearance — your servicer is required by federal regulation to evaluate these options if you apply. Start with a HUD-approved housing counselor, and use the Consumer Financial Protection Bureau's mortgage help resources. The Tennessee Housing Development Agency (THDA) is the HUD-approved state counseling agency and is free.

- Reinstatement. Some loan contracts allow you to bring the loan current up to a certain date before the sale. Tennessee does not require reinstatement by statute outside of high-cost home loans (§ 45-20-104), so check your loan documents.

- Short sale. If the home is worth less than you owe, your lender may approve a sale below the loan balance. This requires lender cooperation and takes time you may not have.

- Deed in lieu of foreclosure. You voluntarily transfer the home to the lender. Saves you the auction but does not generally preserve equity or avoid all credit damage.

- Bankruptcy. A Chapter 13 filing can pause the sale and let you catch up over time. Talk to a Tennessee bankruptcy attorney before deciding — it is a serious step.

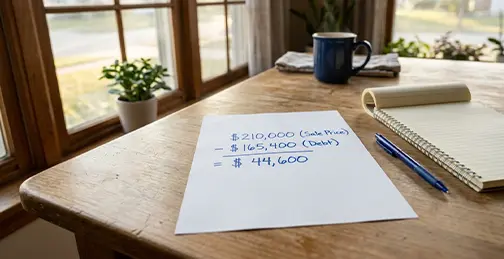

- Sell for cash before the sale date. A direct cash buyer (like Whitley Hamilton Home Buyers) can close in as little as 7–14 days — faster than the trustee's sale clock. The sale pays off the loan, preserves any remaining equity for you, and avoids both the foreclosure mark on your credit and any deficiency exposure that comes with a foreclosed-and-resold property. This is what we do.

What a Cash Sale With Whitley Hamilton Looks Like

- Step 1: Call us or fill out the form. Tell us the property address and roughly where you are in the timeline. There is no pressure, no judgment, and no obligation.

- Step 2: We assess the home as-is. No repairs, no cleaning, no showings, no strangers walking through.

- Step 3: You receive a fair written cash offer, often within 24 hours.

- Step 4: We coordinate with your lender to get a payoff figure and with a licensed Tennessee title company to schedule closing — typically before the trustee's sale date.

- Step 5: At closing, the mortgage is paid off, any remaining equity goes to you, and the foreclosure does not happen. You keep your options open and your credit far less damaged.

Talk to a Neighbor

If a Tennessee foreclosure is somewhere in your timeline, we will give you our honest read on where you actually stand and what your real options are — including ones that are not selling your house to us. Fill out the form or call. People come first.

Get Your Free Offer TODAY!

Fill In This Form To Get Your No-Obligation All Cash Offer Started!

Whitley Hamilton Home Buyers serves homeowners throughout Kingsport, Johnson City, Bristol, Jonesborough, Bluff City, Church Hill, Mount Carmel, Gray, and communities across the Tri-Cities and Northeast Tennessee.